The Federal Reserve begins the brand new 12 months with capital, correctly accounted for, of damaging $92 billion. How can that be? How can the world’s best central financial institution, the issuer of the world’s dominant reserve forex, be technically bancrupt—and by such an enormous quantity?

The reply is that the Fed has gathered immense working losses, which by January 3, 2024, totaled $135 billion. Since September 2022, the Fed has been paying out extra in curiosity expense to finance its greater than $7 trillion securities portfolio than it receives in curiosity earnings. The losses proceed into 2024 on the fee of over $2 billion every week. If you subtract the Fed’s gathered losses, that are actual money losses, from the Fed’s acknowledged capital of $43 billion, you get the Fed’s true consolidated capital, that’s: $43 billion in beginning capital minus $135 billion in losses equals the present capital of damaging $92 billion. This stability sheet math is simple and unassailable underneath typically accepted accounting rules (GAAP).

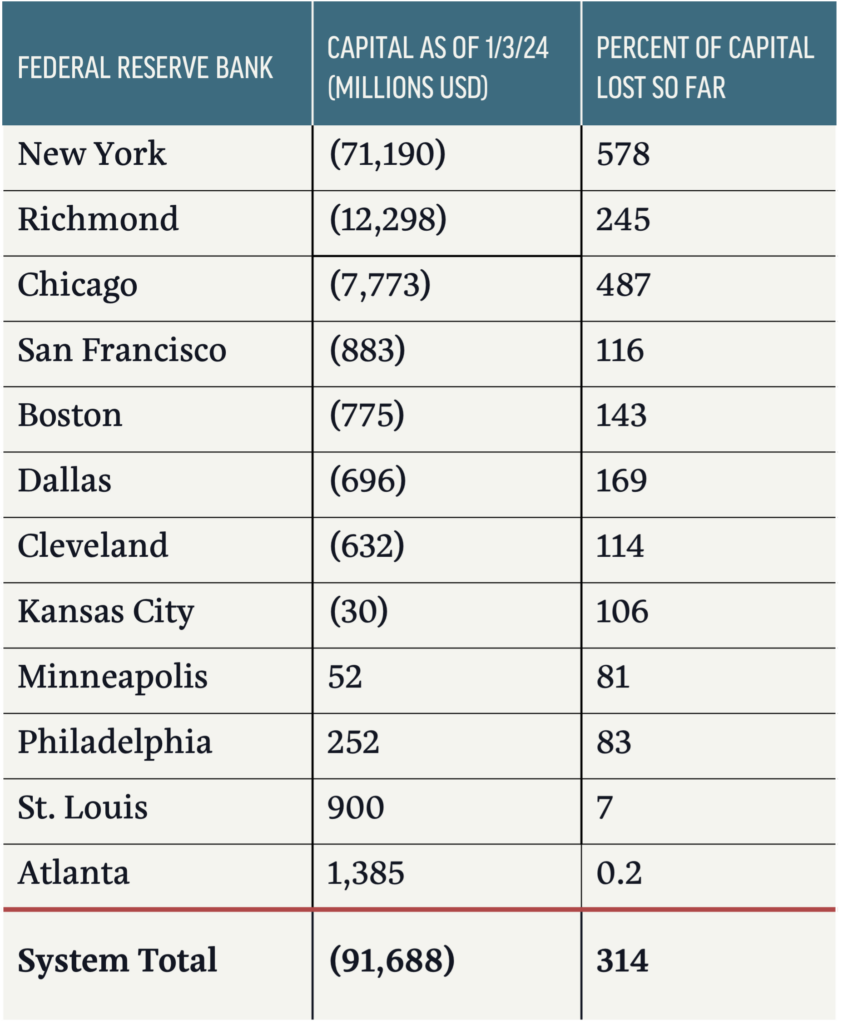

The Federal Reserve System contains 12 regional Federal Reserve Banks (FRBs), each a separate company with its personal shareholders, clients, and stability sheet. Thought-about on their very own, with correct accounting, 8 of the 12 FRBs begin 2024 with damaging capital. This implies their gathered money working losses exceed 100% of their capital. Two others have misplaced greater than 80% of their capital and can exhaust their capital in 2024. Solely two FRBs have their capital intact. Their working losses have been restricted as a result of these banks have an particularly excessive proportion of their funding provided by the paper forex (Federal Reserve Notes) they challenge—forex doesn’t pay curiosity and thus ends in decrease total curiosity expense. Underneath business financial institution guidelines, 10 of the 12 FRBs could be categorised as severely undercapitalized, as would the complete consolidated Federal Reserve System. As of January 3, 2024, the FRBs true capital numbers are:

On the present fee the Fed is shedding cash, its damaging capital will exceed $100 billion by February 2024.

You’ll not discover the Fed’s true capital place reported on the Fed’s official consolidated stability sheet or on the person FRBs’ stability sheets. It’s because the Fed—unbelievably—doesn’t subtract its losses from its retained earnings. As an alternative, it pretends that its rising losses are an asset. “Ridiculous!” you might exclaim. The kindest method to describe this Fed accounting is that it’s non-standard, however Congress has allowed the Federal Reserve to find out its personal accounting guidelines. Since its gathered working losses have made the precise liabilities of the Fed bigger than its belongings, the Fed created a brand new “asset” as a result of it doesn’t wish to present that it has damaging capital. We don’t counsel you do this accounting sleight-of-hand if you’re a non-public financial institution, a enterprise, or filling out a house mortgage software.

The Fed claims that, even when it does have damaging capital, it doesn’t matter as a result of it might all the time print all the cash it wants. Nevertheless, there are, in actual fact, limits to its means to print paper forex. However even when there have been no limits, the Fed’s giant damaging capital, rising ever extra damaging every week, actually makes the Fed look dangerous—incompetent even—and calls its credibility into query. Whereas it isn’t extensively understood, the deposits in FRBs are unsecured liabilities of every particular person FRB. When an FRB has damaging capital, the presumed risk-free standing of its deposits hinges on a perception that the deposits are implicitly assured by the US Treasury.

Sustaining market confidence within the Federal Reserve System and FRBs is crucial. Because the Fed’s losses proceed to quickly accumulate, it will be wise for Congress to recapitalize the Fed and convey it again to constructive capital with belongings larger than, as a substitute of lower than, its liabilities, and restore it to technical solvency. This might be executed with 4 steps, which might match properly with and increase Pollock’s proposals for Reforming the Federal Reserve:

- Droop FRB dividends

- Train the Fed’s present capital name on its stockholders

- Assess the stockholders to offset Fed losses, as supplied within the Federal Reserve Act (FRA)

- Have the US Treasury purchase inventory within the Federal Reserve, in keeping with the unique FRA.

Droop Dividends

When banks or some other firms are struggling big losses, particularly if they’ve damaging retained earnings, not to mention damaging complete capital, a typical and wise response is to cease paying dividends. Certainly, the Federal Reserve in its position as a financial institution regulator would insist on this for the banks and holding corporations it regulates. The identical logic ought to apply to the Fed itself. The central financial institution of Switzerland is an instructive instance. Just like the Fed, the Swiss Nationwide Financial institution is now going through losses however, in contrast to the Fed, it nonetheless has vital constructive capital. Nonetheless, the Swiss Nationwide Financial institution has stopped paying dividends for the final two years. When the Fed is shedding over $100 billion per 12 months, there’s scant justification for it to be paying $1.5 billion in dividends to its member financial institution shareholders yearly.

Nevertheless, to cease a technically bancrupt Fed from paying dividends, Congress has to become involved and amend the Federal Reserve Act. The FRA at the moment supplies that the Fed’s dividends are cumulative. This provision displays the previous perception that the Fed would all the time make earnings. With at present’s actuality of huge losses, the Federal Reserve Act must be revised to make dividends noncumulative and to ban FRB dividend funds if such funds would lead to damaging retained earnings (“surplus” in Fed terminology) on a GAAP foundation.

Train the Fed’s Current Capital Name on its Stockholders

Part 2.3 of the Federal Reserve Act requires each financial institution that could be a member of a Federal Reserve Financial institution to subscribe to shares of the FRB in an quantity tied to the member financial institution’s personal capital. The member-stockholders, nevertheless, are required to pay in and have paid in solely half of the quantity subscribed. The opposite half is topic to name by the Federal Reserve Board, and if referred to as, should be paid in by the member financial institution.

The full paid-in capital of the Fed is $36 billion. An extra $36 billion in FRB capital might be raised if the Federal Reserve Board merely exercised its present statutory name. This would scale back the Fed’s damaging capital as of January 3, 2024, by 39%. If the Federal Reserve Board balks at exercising the capital name, Congress ought to instruct it to take action.

Underneath our really useful modifications to Fed dividend coverage, the newly paid-in shares wouldn’t obtain dividends till FRBs return to constructive GAAP retained earnings (“surplus”).

Assess the Stockholders to Offset Fed Losses, as Offered for within the Federal Reserve Act

In a really little-known however essential provision of the FRA, which matches again to its unique 1913 enactment, Federal Reserve Financial institution shareholders are made liable along with their subscription to Fed inventory, for an additional quantity equal to that subscription, which they could be assessed to cowl all obligations of their FRB; in different phrases, to offset damaging capital. A member financial institution evaluation could be a money contribution to their FRB, not an funding in additional inventory. Says the FRA, “The shareholders of each Federal reserve financial institution shall be held individually accountable … to the extent of the quantity of their subscriptions to such inventory on the par worth thereof along with the quantity subscribed.” (Italics added.)

The full subscriptions to Fed inventory are twice the excellent paid-in capital of $36 billion, so the subscriptions complete $72 billion, and the utmost potential evaluation on the Fed member banks is thus $72 billion. Since two FRBs, Atlanta and St. Louis, nonetheless have their capital intact, the obtainable evaluation could be on the opposite ten FRBs. The utmost assessments could be these FRBs’ paid-in capital of $34 billion occasions 2, or $68 billion. By comparability, the Fed paid $177 billion in curiosity and dividends to its member banks in 2023.

The unique Federal Reserve Act, as enacted in 1913, supplied for the US Treasury to purchase Federal Reserve Financial institution inventory, if needed.

With the utmost evaluation on the members of those ten FRBs along with calling the unpaid half of the inventory subscriptions for all of the FRBs, the overall raised could be $104 billion ($36 billion in new inventory plus $68 billion in assessments). This quantity would offset the Fed’s year-end capital deficit of $92 billion and would cowl about six weeks of further losses on the present fee of $2 billion every week.

Probably the Fed’s member banks could be exceedingly sad with these actions to shore up the capital of the Federal Reserve. However member banks, as the only real shareholders within the FRBs, have a transparent statutory obligation to financially help FRBs that may quickly have consolidated true damaging capital in extra of $100 billion.

Judging by public monetary statements disclosures, few—if any—Fed member banks have significantly thought of the big statutory contingent legal responsibility that membership within the Fed brings. Taking into consideration FRBs’ monetary situation and their shareholders’ clear authorized obligations, it appears that evidently FRB member banks must be disclosing this materials contingent legal responsibility.

Have the US Treasury Purchase Inventory within the Federal Reserve, According to the Unique Federal Reserve Act

Suspending FRB dividends, calling the remainder of the member banks’ inventory subscriptions, and assessing FRB stockholders the utmost quantity would make the Fed’s capital constructive once more till mid-February 2024. After that, persevering with losses will put it again into damaging territory and the Fed again into technical insolvency. Given the truth that the Fed is caught with long-term fixed-rate investments yielding a mere 2%, and that $3.9 trillion of its investments have greater than ten years left to maturity, the Fed’s very giant money losses will probably proceed for fairly some time.

One other supply of recapitalization is required.

The unique FRA as enacted in 1913 supplied for the US Treasury to purchase Federal Reserve Financial institution inventory, if needed. (It additionally supplied for potential sale of FRB inventory to the general public, which didn’t occur and couldn’t occur underneath at present’s circumstances.) Part 2.10 of the FRA, which has by no means been amended, empowers an FRB to challenge shares to the Treasury to lift wanted capital:

Ought to the overall subscriptions … to the inventory of stated Federal reserve banks, or any a number of of them, be, within the judgment of the group committee [the Secretary of Treasury, the Secretary of Agriculture, the Comptroller of the Currency], inadequate to supply the capital required therefor, then and in that occasion the stated group committee shall allot to the US such an quantity of stated inventory as stated committee shall decide. Stated United States inventory shall be paid for at par out of any cash within the Treasury not in any other case appropriated, and shall be held by the Secretary of the Treasury, and be disposed of… because the Secretary of the Treasury shall decide.

In a 1941 opinion, the Federal Reserve Board argued: “As initially enacted, the Federal Reserve Act supplied for a Reserve Financial institution Group Committee … [and] was approved to allot Federal Reserve Financial institution inventory to the US within the occasion that subscriptions to such inventory … had been insufficient. Nevertheless, subscriptions by member banks had been ample. … Accordingly, [this section] is now of no sensible impact.”

Nevertheless, the Fed’s monetary situation has dramatically modified since 1941. In 2024, the subscriptions to the capital of the FRBs are grossly insufficient—the FRBs can’t preserve constructive capital. Allocation of Fed inventory to the US would now be of very vital sensible impact.

In mild of the Fed’s technical insolvency, ongoing big losses, and massively damaging capital, Congress may sensibly amend Part 2.10 to learn as follows:

Ought to the overall subscriptions to the inventory of the Federal reserve banks and the additional assessments of the shareholders be inadequate to take care of constructive capital as measured by GAAP for any a number of of the Federal reserve banks, then the Board of Governors of the Federal Reserve shall allot to the US such an quantity of stated inventory because the Board shall decide will carry the capital as measured by GAAP of those Federal reserve banks to not lower than $100 million and preserve the consolidated capital of the Federal Reserve System as measured by GAAP at not lower than $1.2 billion. The USA inventory shall be paid for at par out of any cash within the Treasury not in any other case appropriated and shall be held by the Secretary of the Treasury. Stated inventory could also be repurchased at par by a Federal reserve financial institution or banks at any time, supplied that after the repurchase, the capital of every Federal reserve financial institution as measured by GAAP shall be not lower than $100 million and that the consolidated capital of the Federal Reserve System as measured by GAAP shall be not lower than $1.2 billion.

The inventory bought by the Treasury could be non-voting, because the FRA supplies that “Inventory not held by member banks shall not be entitled to voting energy.”

If over the following 15 months the Fed loses the identical $135 billion because it has within the final 15 months, the Treasury would personal about $123 billion in par worth of FRB inventory by March 31, 2025, and the member banks would personal $72 billion after the capital name. The Treasury would thus personal about 62% of the consolidated Fed inventory however couldn’t vote its shares. Over the long-term future, the FRBs would repurchase the Treasury’s shares as their funds allow.

With these 4 steps, the recapitalization of the Federal Reserve could be full. Our proposed consolidated capital of $1.2 billion in comparison with the Fed’s starting of 2024 complete belongings of $7.7 trillion, would give the Fed a leverage capital ratio of 0.016%—small certainly, however all the time constructive. In different phrases, this revised part of the Federal Reserve Act would imply that the Treasury would, because it does for Fannie Mae and Freddie Mac, make sure that over time, crucial central financial institution on the earth would by no means once more be technically bancrupt, regardless of how huge its losses.