Do you’ve gotten a favourite sauce? One in every of mine is a candy chili sauce that I take advantage of on salmon, cucumber salad, and different recipes. Most everybody has a favourite sauce or a dip, with a couple of hundred varieties to select from. You might like a selected marinara, tzatziki, or tahini. You might fancy a chutney, wasabi, soy, or sriracha. Whether or not you want béchamel, béarnaise, or barbecue, there’s undoubtedly some sort of sauce that you just periodically simply crave.

The unusual factor about sauces, although, is that they’re meals, however they aren’t a meal. They aren’t soup. They aren’t interesting on their very own. They’re merely meant to be “meals assist.” They complement and improve. Sauces aren’t the factor. They get added to the factor to make it higher. All the things tastes somewhat higher with the correct of sauce.

It’s the similar with knowledge. Information isn’t the factor. It’s essential and might make or break your insurance coverage operation. However knowledge is a key supporting participant, an integral a part of the merchandise, companies, and experiences it enhances.

Information is the lifeblood of insurance coverage and the important thing to unlocking the ability and potential in a lot of what insurers do. Information is the important thing to underwriting established merchandise correctly. It’s the important thing to creating new merchandise primarily based on new markets and newly out there knowledge sources. It’s the important thing to profitable the revenue sport. It’s the important thing to determine fraud. There’s nearly nowhere in insurance coverage that gained’t enhance if you understand how to use knowledge in the correct method. In insurance coverage, every little thing goes higher with knowledge.

The issue is that many insurers are having hassle getting the sauce out of the kitchen. They’ve a few of the proper elements. They’ve some inspiration. They’ve a couple of recipes of their field. However, they’re stymied on how one can make one thing magnificent out of the bits and items that appear like they could go properly collectively.

It was once, with knowledge, the time it took to determine it out didn’t matter a lot. Insurers might take their time, create their fashions, and run some numbers. Insurers might spend years and years turning knowledge into improvement, however that’s not doable in the present day. Property insurers, particularly, are in a spot the place they MUST get their knowledge and analytics working for them shortly, or it gained’t be working in any respect.

The actual reply within the knowledge sport is to determine the place the information could also be utilized, the place it can have probably the most affect, and do the perfect. Majesco, the truth is, has already carried out this evaluation many occasions over and is utilizing these insights in our options for the trade. We’ve discovered, time and time once more, that the alternatives for insurers are discovered within the gaps between what is anticipated by prospects and what’s at present in vogue for insurers. When insurers catch as much as prospects, they fill the gaps, and on this case, that signifies that insurers can be utilizing knowledge and analytics in a manner in that can positively affect each their prospects and their inside operations. In case you’d like to grasp these gaps in larger element, it is best to learn Majesco’s current survey report, Bridging the Buyer Expectation Hole: Property Insurance coverage.

Why rush the information and analytics recipe?

The state of the property insurance coverage enterprise is more and more difficult. It wants a change of operations and know-how that makes use of knowledge intelligently to stay viable and worthwhile. 2022’s pure disasters had a huge effect on the trade. However 2023 is worse. Based on the newest NOAA report, the US skilled 23 separate billion-dollar climate and local weather disasters within the first 8 months of 2023 – the most important quantity since information started and already surpassing the earlier report of twenty-two occasions in 2020. And this was earlier than the newest hurricanes and with 4 months to go in 2023.

The rising variety of excessive climate occasions and pure disasters has had a considerable impact on individuals and companies. With rising property costs, supplies, and restore prices, many insureds lack ample insurance coverage protection, leading to a spot and elevated monetary threat.

The affect of that is that property disaster reinsurance charges are rising. The January 2023 renewals mirrored 20-year highs, persevering with a trajectory that started in catastrophe-exposed property versus non-catastrophe uncovered property, resulting in huge worth variations. Demand for protection has grown as pure disasters proceed to affect prospects and insurers alike. However different elements akin to inflation, provide chain challenges, dramatic property worth will increase, and monetary market losses are driving the trade additional into a tough market. This development is solidified by the American Property and Casualty Insurance coverage Affiliation noting in a 2023 report, that the mix of historic excessive inflation and the rising frequency of pure catastrophes has created the toughest market in a technology for property insurance coverage.[1] We will probably anticipate excessive charges once more for 2024 renewals given what has occurred this yr.

What’s the answer?

Insurance coverage losses are leading to increased premiums for patrons, increased premiums for reinsurance for insurers, and a refocus on the underwriting self-discipline, new merchandise, and value-added companies that concentrate on threat resiliency with prevention and mitigation.[2]

So, the place can any insurer discover alternative within the mild of an surroundings that begs for adaptation and innovation?

Nicely, there’s knowledge. Industrial property buildings, for instance, are more and more changing into “sensible” and delivering huge quantities of knowledge by means of real-time related gadgets built-in with Constructing Administration Techniques (BMS) that can be utilized to watch, predict, and stop loss. Along with defending the constructing surroundings from dangers akin to water leaks, hearth, or equipment put on, sensors can assess exterior dangers akin to climate, to offer a 360-degree view of threat in real-time.

And there’s loss management – both with adjusters or utilizing digital capabilities like video and self-surveys to seize footage, knowledge, and different details about properties – each business and private after which assess that knowledge for threat.

Each of those are a chance, and due to the proliferation of sensor and sensible applied sciences, digital loss management capabilities like Majesco Loss Management, to not point out the brand new applied sciences akin to ChatGPT and actionable AI, there are numerous extra alternatives identical to it.

The adage of “management what you’ll be able to management” is now entrance and middle for insurers as they take a look at new threat administration methods as a vital part of their buyer technique and their property strains of enterprise. Insurers should more and more focus their time and sources on how they’ll higher assess threat for a broader set of properties and stop losses to enhance underwriting profitability and buyer experiences. The answer will contain knowledge, superior analytics, and different instruments that harness knowledge’s energy, however the answer will solely be viable for insurers who’re keen to catch up, proper now. Information will stretch insurers and their capabilities, however it can stretch them in the correct path, getting ready them for a way more environment friendly and worthwhile future.

Information & Analytics for Property Pricing and Underwriting

P&C underwriting is on the coronary heart of the insurance coverage enterprise. From evaluating particular person dangers and the exposures in a whole portfolio to assessing the chance, threat urge for food, and in the end profitability, underwriting is more and more essential within the face of quickly altering threat elements. On the core of underwriting is knowledge.

Insurance coverage has all the time been a data-driven enterprise, however entry to new knowledge sources for properties and using AI/ML is redefining and revolutionizing the trade. Danger administration, underwriting, and loss management all contain gathering and utilizing knowledge wanted for AI/ML fashions to precisely assess and determine threat, and handle and scale back dangers.

Majesco has the trade’s most in depth repository of property loss management survey knowledge, encompassing over 2 billion observational knowledge factors from 16+ million meticulously accomplished property surveys carried out by skilled threat engineers within the subject. These surveys, rigorously quality-assured, embody a staggering 200+ million tagged pictures, offering the perfect basis for harnessing the potential of AI/ML. We’ve used this knowledge to develop our Property Intelligence AI/ML mannequin to assist assess particular property knowledge utilizing this repository of knowledge. Utilizing this knowledge and our mannequin, insurers can personalize the pricing and underwriting for the shopper’s particular threat.

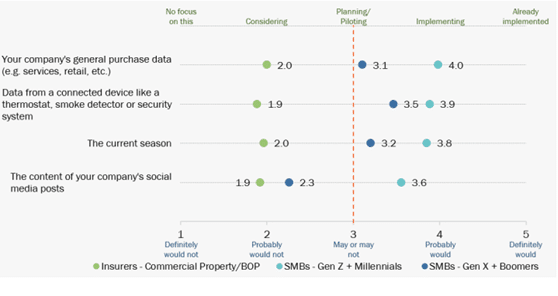

Industrial Property SMB – Insurer Gaps in Information Use and Curiosity

Keep in mind when insurance coverage’s excuse for not utilizing knowledge was that prospects didn’t wish to hand over their key bits of related knowledge, even when it meant that it might save them cash? Who might need guessed that the problem has flipped and that now it might be that insurers might lose enterprise as a result of prospects are keen to share the information and insurers aren’t able to make a buyer’s knowledge work for them.

Based on Majesco surveys, the previous excuse evaporated within the business market. Overwhelmingly, SMBs are keen to share knowledge with insurers to cost and underwrite their business property insurance coverage at almost double the speed that insurers are at present utilizing this knowledge, as mirrored in Determine 1. Apparently, each generational teams agree, aside from social media content material, the place the older technology aligns with insurers.

Determine 1: Buyer-Insurer gaps in new knowledge sources and applied sciences for business property insurance coverage pricing and underwriting

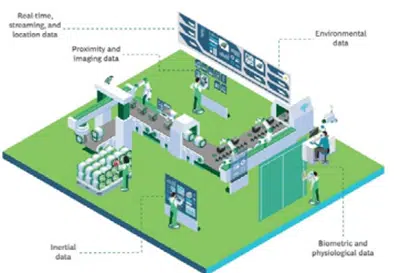

The expansion of IoT gadgets and sensors all through houses and companies is accelerating. Along with sensors (temperature, water, infrared, sound, and so on.), we’re witnessing great development in video surveillance (with cell capabilities), significantly given the rise in crime because of societal threat.

Based on a BCG article, in 2020 there have been 30 billion related gadgets on the planet, which is anticipated to extend by over 30%, to 41 billion gadgets by 2024.[3] As we speak’s IoT gadgets embedded in gear and infrastructure for business companies produce over 14 zettabytes of knowledge, with numerical or visible data on individuals, issues, and environmental elements, as mirrored in Determine 2. The breadth of this knowledge provides the chance to make use of it in real-time, reasonably than depend on historic knowledge for threat evaluation and underwriting, whereas additionally offering new knowledge that provides extra perception into the chance.

Determine 2: Forms of knowledge generated by business IoT gadgets

In truth, companies are making the most of IoT-based applied sciences to streamline processes, improve effectivity and security, and supply safety. It’s estimated that just about 34% of North American and European companies use IoT gadgets, with one other 12% planning to combine IoT throughout the subsequent yr.[4]

Insurers’ capability to create buyer worth from the IoT will depend upon their willingness to dive in and begin experimenting with IoT know-how and knowledge in the present day. Leaders are doing this and can outpace those that observe, placing them liable to conserving their prospects. Insurers that want to stay viable, should catch up of their use of knowledge within the business market.

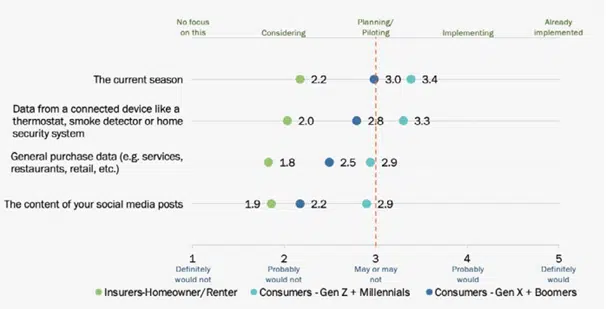

Private Property Client – Insurer Gaps in Information Use and Curiosity

Just like SMBs, customers are overwhelmingly interested by utilizing their knowledge for pricing and underwriting of their property insurance coverage as mirrored in Determine 3. In truth, they’re as much as 2 occasions extra than insurers, reflecting a big buyer expectation hole.

Determine 3: Buyer-Insurer gaps in new knowledge sources and applied sciences for private property insurance coverage pricing and underwriting

Based on CoreLogic’s Residential Value Handbook, almost 64% of householders don’t have sufficient insurance coverage protection and are underinsured by a mean of 27%.[5]

This isn’t stunning, given the rise in property values. In November 2021, it was reported that the median worth of single-family current houses rose in 99% of the 183 markets tracked by the Nationwide Affiliation of Realtors within the third quarter, with double-digit worth will increase seen in 78% of the markets.[6]During the last couple of years, costs have risen from 15% to over 30% on common, with some markets even increased. Think about doing a digital loss management survey by way of self-survey or video in your total guide of enterprise to higher assess every property threat, but in addition to higher assess reinsurance wants. Majesco has prospects who’re doing simply that with nice success.

Including gas to the change, it’s anticipated that sensible house gadgets will proceed to be a significant space for IoT, with over 800 million sensible house gadgets shipped in 2020 and predicted to exceed 1.4 billion by 2025. It’s estimated that 41.9% of US households owned a sensible house gadget in 2021, which is able to rise to almost 50% by 2025. The result’s the variety of sensible house gadgets bought will exceed 1.94 billion by 2023.[7]

This development in adoption provides insurers a big alternative to satisfy buyer expectations by capturing and utilizing the information for customized threat assessments and underwriting. With the elevated valuations and the expansion of the adoption of sensible house gadgets, prospects are more and more interested by customized pricing and underwriting primarily based on their very own location and property particulars. Insurers should start to handle this want and expectation to accumulate and retain prospects. Buyer loyalty is in jeopardy as soon as customized pricing takes over the market. Solely insurers which can be assembly expectations can anticipate to hold on to and broaden their enterprise and portfolio of consumers.

However greater than that, solely insurers who actually perceive their enterprise, utilizing knowledge as their information, will know which enterprise they need and which they don’t need. The information-smart insurer will profit from the data-vetted portfolio.

Majesco is, proper now, serving to insurers to transition their operations to catch up within the knowledge sport. These corporations are getting ready to make the most of market-leading knowledge and analytic applied sciences for P&C insurance coverage. They’re making higher choices utilizing knowledge and analytics and are proving how every little thing within the insurance coverage operation goes higher with knowledge. Majesco’s Clever Core for P&C, Loss Management, and Property Intelligence is at the forefront of what main insurance coverage operations want now, and within the very close to future.

“The necessity for fast product innovation, environment friendly operations, and strong digital capabilities is driving the necessity for core methods wealthy with APIs and accessible knowledge. Majesco provides a P&C Coverage answer with an open structure and self-service configuration instruments that allow insurance coverage carriers to deploy the capabilities wanted to achieve this new period of insurance coverage. Majesco’s sizable buyer base and continued momentum available in the market qualifies them as a Dominant Supplier within the P&C core methods house.” — Martina Conlon, Head of Property and Casualty Insurance coverage at Datos Insights.

Do you perceive what it means to have an Clever Core and superior knowledge and analytics operating your small business? Take a look at Majesco’s newest webinar, The Daybreak of Clever Core Insurance coverage Software program, for a peek at how knowledge and AI/ML, working collectively, will rewrite the foundations of P&C insurance coverage.

[1] Sams, Jim, “APCIA Says Property Insurance coverage Market ‘Hardest in a Era’,” Claims Journal, March 28, 2023, https://www.claimsjournal.com/information/nationwide/2023/03/28/316110.htm

[2] “Details + Statistics: Householders and renters insurance coverage,” Insurance coverage Info Institute, https://www.iii.org/fact-statistic/facts-statistics-homeowners-and-renters-insurance

[3] Taglioni, Giambattista, et al., “The Energy of the Web of Issues in Industrial Insurance coverage,” BCG, October 4, 2021, https://www.bcg.com/publications/2021/commercial-insurance-should-start-testing-the-power-of-the-internet-of-things

[4] Vailshery, Lionel Sujay, Web of Issues (IoT) within the U.S. – statistics & info, Statista, October 27, 2022, https://www.statista.com/matters/5236/internet-of-things-iot-in-the-us/

[5] “Report: How Many US Houses Are Underinsured?” Kin, April 12, 2021, https://www.kin.com/weblog/underinsurance-report/

[6] “Residence Costs Spiked In Practically All Metro Areas In 3Q 2021,” Nationwide Mortgage Skilled, November 12, 2021, https://nationalmortgageprofessional.com/information/home-prices-spiked-nearly-all-metro-areas-3q-2021

[7] Cook dinner, Sam, “60+ IoT statistics and info.” Comparitech, December 13, 2022, https://www.comparitech.com/internet-providers/iot-statistics/