Argentina welcomes a brand new president. Defying ballot predictions of a technical tie, the anarcho-capitalist candidate Javier Milei achieved a powerful victory over Peronist Sergio Massa within the runoff by a large margin. The sudden flip of occasions led to Massa conceding defeat even earlier than the official outcomes had been introduced, shocking many observers.

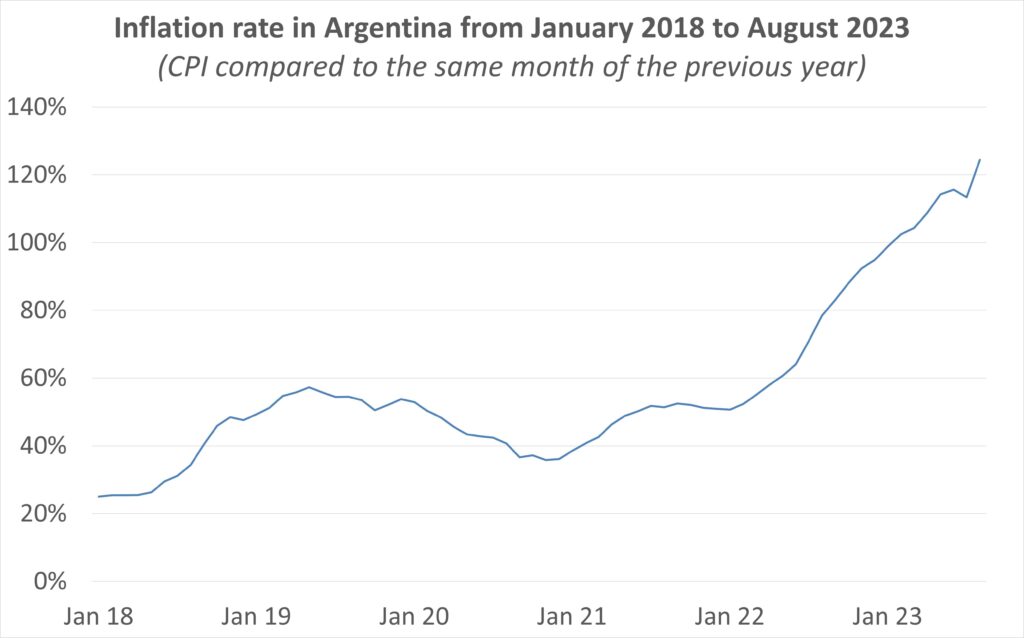

Because the president-elect, Milei will confront 4 speedy financial challenges: addressing inflation, curbing the fiscal deficit, eliminating regulatory hurdles that hinder the expansion of the Argentine financial system, and tackling elevated poverty charges. Essentially the most urgent concern is the looming threat of hyperinflation. Inflation has plagued Argentina for many years, constituting an everlasting financial ailment. From 1980 to 2022, the nation skilled an common inflation charge of 206%. During the last twelve months, costs surged by a staggering 143%.

Milei’s plan to sort out inflation hinges on the unconventional step of dismantling Argentina’s central financial institution (BCRA) and embracing the US greenback because the nation’s official forex. This proposition has sparked fervent debate, evident within the robust resistance it faces from politicians throughout the political spectrum and distinguished teachers. Nonetheless, there’s a widespread acknowledgment that decisive motion should be taken to confront the nation’s foremost financial problem. Does dollarization signify the optimum technique to set the nation on a path towards financial stability?

There is no such thing as a easy reply. Dollarization isn’t the primary most suitable option, because it deprives central banks of the financial coverage instruments they usually make use of to deal with financial crises. As an illustration, within the face of deflationary pressures, a central financial institution would usually cut back the coverage charges to stimulate financial exercise. In a dollarized financial system, the nationwide central financial institution is both eradicated (as Milei proposes) or loses its authority over financial coverage, leaving policymakers with fewer sources to make use of within the occasion of a disaster.

Moreover, the elimination of the BCRA implies the lack of its position as a lender of final resort to deal with liquidity points inside the banking sector, particularly throughout monetary crises. Likewise, the method of dollarization calls for an ample provide of greenback reserves, and the BCRA has notably diminished its holdings over the previous 12 months. This discount in reserves might probably introduce issues within the dollarization course of. The query then arises: are these challenges insurmountable?

Undoubtedly, the perfect stance for a rustic or a bunch of nations is to uphold financial coverage autonomy. Nonetheless, the effectiveness of such a coverage hinges on the existence of an unbiased central financial institution endowed with the capability to advertise worth stability by way of considered financial measures. This stands in distinction to the BCRA, which has demonstrated a dismal observe report in controlling inflation, as evidenced by the recurring inflationary episodes over the previous many years.

A much less radical plan of action might contain retaining the peso whereas endowing the BCRA with independence from political interference, thereby curbing its tendency to monetize authorities debt. Regrettably, this feature is perhaps hindered by the BCRA’s lack of credibility and the historic lack of ability of politicians over the previous many years to successfully tackle and management inflation by granting independence to Argentina’s central financial institution.

Can the banking system survive with out a central financial institution injecting liquidity when required? Within the absence of a central financial institution, banks would possibly search various avenues for liquidity, comparable to establishing partnerships with international banks or participating with worldwide monetary establishments—a method beforehand noticed in dollarized economies. This exterior involvement not solely has the potential to offer an alternative choice to the absent central financial institution assist but additionally introduces a mechanism for instilling self-discipline inside the banking system.

The essential concern that looms giant revolves across the inadequate greenback reserves on the BCRA, that are a prerequisite to dollarizing the Argentine financial system. This might hinder, delay, and even derail Milei’s dollarization plans, forcing him to discover options to sort out inflation. Milei’s administration has the potential to get rid of alternate charge controls and facilitate the influx of {dollars}. Nonetheless, the problem lies in executing this transfer abruptly with out addressing fiscal imbalances, because it might result in a considerable depreciation of the peso and, consequently, set off hyperinflation. A extra wise answer might contain in search of further reserves by borrowing from the IMF or worldwide banks.

The execution of Milei’s dollarization plan attracts inspiration from Emilio Ocampo and Nicolas Cachanosky’s e-book, Dolarización: Una Solución para la Argentina. Ocampo is even anticipated to be BCRA chairman beneath Milei’s administration. The plan contains three phases. First, peso-denominated financial institution deposits are reworked into {dollars} at a predetermined fastened alternate charge, which might coincide with the market charge. It’s vital to notice that, for dollarization to achieve success, banks usually are not required to carry the whole nominal worth of deposits in greenback reserves. They need to merely preserve enough reserves within the central financial institution to cowl buyer money withdrawals and fulfill different monetary obligations, simply as they do right this moment. Concurrently, loans and different monetary property on banks’ stability sheets are transformed into {dollars}, permitting any new influx of {dollars} into the banking system to facilitate this transition.

The second part entails the conversion of the circulating pesos into {dollars}. The best strategy is to encourage people to deposit their peso-denominated banknotes into their accounts, the place they might be routinely transformed into {dollars}. Alternatively, it might contain authorizing particular places of work to facilitate the alternate of pesos for {dollars} at a hard and fast alternate charge inside a chosen timeframe. In both state of affairs, the BCRA wouldn’t be required to carry the whole sum of greenback reserves upfront.

The ultimate part represents essentially the most intricate stage of the method, because it entails the conversion of the most important monetary obligation on the BCRA’s stability sheet—particularly, the Leliqs, that are liquidity payments issued by the central financial institution for conducting open market operations. Presently, these Leliqs, constituting roughly 43% of the overall liabilities, reside on the stability sheets of banks. In essence, Ocampo and Cachanosky suggest the institution of a Financial Stabilization Fund (MSF) with the first goal of step by step liquidating these Leliqs. The MSF’s stability sheet would primarily comprise the BCRA authorities bond portfolio and different property (to be extra exact, the prevailing non-transferable bonds on the central financial institution’s stability sheet must be exchanged for a freshly issued set of dollar-denominated bonds, sustaining each their unique nominal values and current values). The revenue generated from these property can be utilized for the aim of step by step retiring the Leliqs.

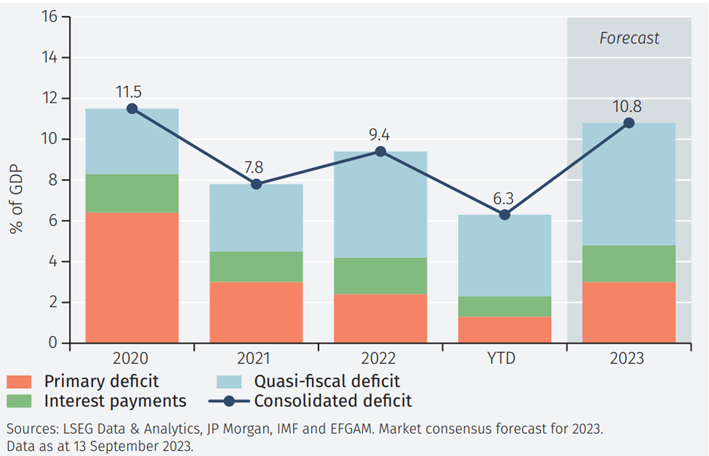

The second problem entails tackling the consolidated fiscal deficit, projected to exceed 10% of GDP in 2023. This consolidated fiscal deficit encompasses the first deficit, curiosity funds, and the quasi-fiscal deficit, which incorporates the interest-bearing liabilities of the BCRA. Milei has promised to chop down wasteful spending to be able to diminish the first deficit with out compromising the standard of presidency providers.

Reaching this aim seems difficult, provided that a good portion of presidency spending is allotted to important areas comparable to schooling, healthcare, and different public providers. And eradicating some authorities departments, as Milei proposes, is not going to save a lot cash for the Argentine treasury. Nonetheless, the proposed dollarization plan might play a vital position in addressing the quasi-fiscal portion of the consolidated deficit over the long run by resolving the problems related to the Leliqs.

Consolidated Fiscal Deficit

A 3rd problem revolves across the regulatory burdens weighing down the Argentine financial system. The newest OECD Financial Coverage Reforms report highlights low productiveness as a result of an absence of home and exterior competitors, excessive commerce boundaries, and an elevated tax burden for enterprise, all of which impede financial development. Moreover, Argentina occupies the 126th place within the Ease of Doing Enterprise rating elaborated by the World Financial institution, and its labor market is characterised by a sizeable casual sector (round 50% of the labor power) coupled with a decline in actual wages over the past years.

On this context, Milei has proposed a collection of loosely outlined reforms with the target of unilaterally opening the financial system to worldwide commerce, lowering taxes, and restructuring the labor market. Nonetheless, he’s prone to encounter vital challenges in implementing these reforms as a result of an absence of majority assist within the Chamber of Deputies.

Lastly, Milei’s administration faces the urgent problem of addressing Argentina’s escalating poverty charges. From 2016 to the current, the nationwide poverty charge has surged from 30% to surpass 40%, leaving roughly 12 million Argentinians struggling under the poverty line. 1 / 4 of this demographic contains unsheltered people.

Whereas the last word answer lies in fostering inclusive financial development by way of financial reforms, speedy measures are crucial. Milei should maintain or develop focused packages particularly designed to alleviate poverty, recognizing the urgency of offering reduction to these most affected by these distressing statistics. Equally, curbing inflation, which particularly impacts the bottom deciles of the revenue distribution, is a positive approach to lower poverty ranges.

The financial scenario in Argentina is essential, and it might deteriorate additional if Milei fails to steer the scenario promptly. The important thing to success hinges on restoring financial stability and stopping a recurrence of hyperinflation. If the brand new authorities can assert management over inflation by way of dollarization, the probability of efficiently addressing different challenges and steering the financial system again heading in the right direction will considerably enhance. Failure to take action will possible seal the destiny of Milei’s administration.