A brand new report from market intelligence agency CONTEXT has highlighted stagnating “industrial” 3D printer shipments throughout Q3 2023.

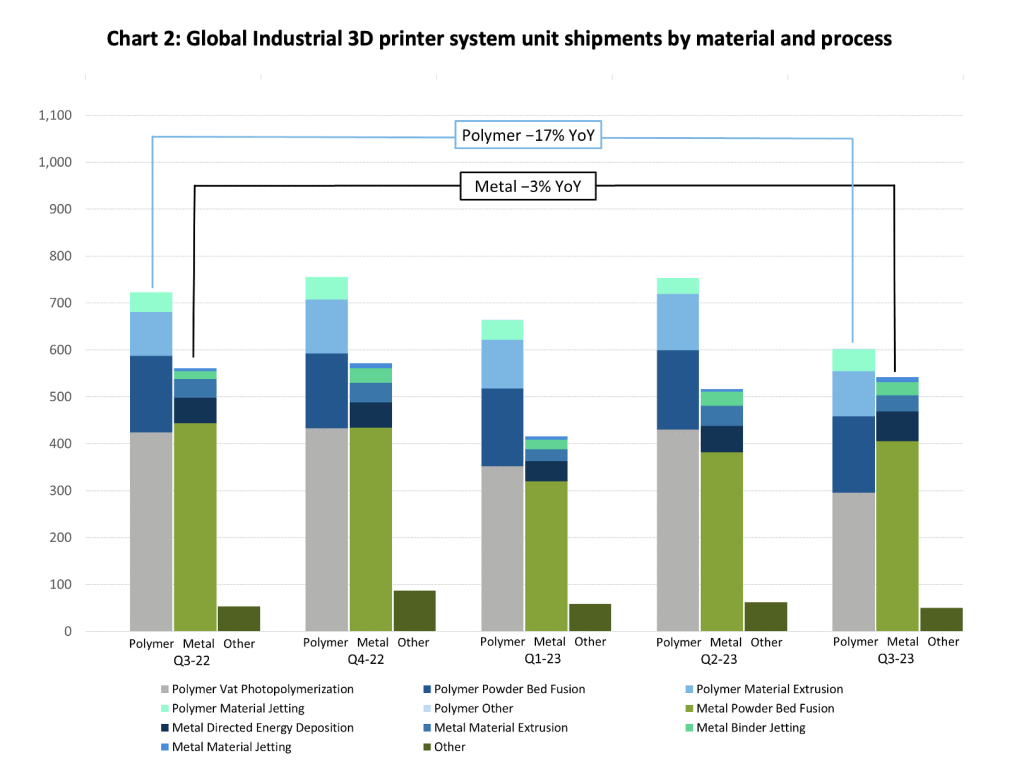

World Industrial polymer 3D printer shipments fell 17% YoY, with steel system shipments experiencing a 3% decline in comparison with Q3 2022. This decline has reportedly been pushed by inflation and excessive rates of interest which can be impacting key markets.

Failed merger and acquisition exercise from the likes of Stratasys, 3D Techniques, Desktop Metallic, and Nano Dimension, together with elevated layoffs, additionally led to a shifting focus away from market progress in direction of profitability.

Nevertheless, entry-level 3D printers proceed to be the quickest rising phase throughout the 3D printing trade, cannibalizing the gross sales {of professional} programs. The current rise of Shenzhen-based desktop 3D printer producer Bambu Lab has contributed to this accelerated progress, with fellow Chinese language firm’s Creality and Elegoo additionally main this market. The decline within the “skilled” phase can definitely be seen as linked to options showing on sub-$2500 3D printers that have been beforehand unavailable.

CONTEXT additionally revealed that, based mostly on rolling five-year international cargo charges, 8.1 million polymer FDM 3D printers have been shipped in that interval. Information from Filamentive’s Materials Sustainability Survey discovered the median filament use was 2kg per thirty days or 24kg per yr. Mixed with CONTEXT knowledge, this means probably 194,400 tonnes of filament yearly, a worth within the area of $3.9 billion.

“Many public 3D printing corporations within the West started shifting their consideration from market progress to profitability and have not too long ago been distracted by failed mergers and layoffs,” defined Chris Connery, head of worldwide evaluation at CONTEXT.

“Though these woes have been mirrored within the wider international market as effectively, there have been pockets of alternative and glimpses of power in some 3D printer segments, particularly within the often-overlooked Entry-level portion of the market.”

The chart under means that 2.7 million 3D printers have been offered throughout all classes through the twelve months main as much as Q3’23. “Of the manufacturers tracked CONTEXT exhibits simply over 2M entry-level (under $2,500) FDM 3D printers have shipped globally within the final 4-quarters from This fall-22 by way of Q3-23,” stated CONTEXT.

Industrial 3D printer shipments fall in Q3 2023

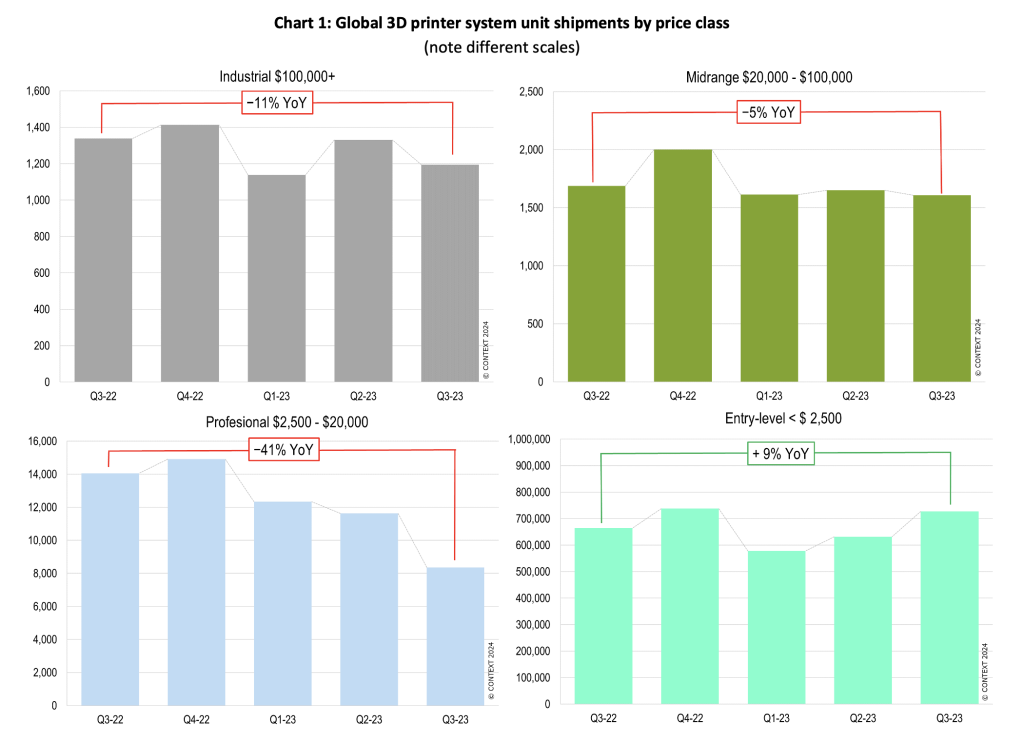

CONTEXT experiences that, throughout Q3 2023, international shipments of Industrial 3D printers costing greater than $100,000 dropped by 11% YoY. A 17% decline was witnessed within the Industrial polymer 3D printer phase, with a 3% drop for Industrial steel 3D printers.

The most important marketplace for this price-class of Industrial 3D printers is inside China. Shipments of such 3D printers to China declined by 16% in comparison with the identical interval in 2022, primarily attributable to weak polymer-based system shipments. Vat photopolymerization 3D printers carried out particularly poorly, with this being the biggest class throughout the Industrial polymer area. If vat photopolymerization programs are excluded, Industrial polymer 3D printer shipments grew 2% YoY.

CONTEXT highlights that these poor cargo figures proceed to be influenced by the financial results of the COVID-19 pandemic. Weak demand inside sure dental markets contributed to the poor outcomes of corporations equivalent to 3D Techniques.

SLA 3D printer producer UnionTech, an Industrial 3D printing market chief, has skilled ‘lumpy and inconsistent’ ends in Q3 2023. The corporate’s Industrial shipments fell by 28% in comparison with 2022, when the corporate was experiencing accelerated restoration from the Shanghai lockdowns.

Nevertheless, some pockets of progress have been highlighted throughout the PBF polymer 3D printer phase. EOS, one of many largest corporations on this class, reportedly skilled ‘glorious’ cargo progress for such programs. Moreover, Stratasys witnessed an 11% YoY improve within the cargo of Industrial polymer 3D printers.

In the end, regardless of total cargo decline, Q3 2023 noticed international Industrial 3D printer revenues improve by 2% YoY.

Cargo decline and income progress in steel 3D printers

In response to CONTEXT, the three% decline in Industrial steel 3D printer shipments was largely pushed by a 9% cargo fall in powder mattress fusion (PBF) programs. CONTEXT calls PBF 3D printers the biggest and most strategically essential class of 3D printers throughout the Industrial steel 3D printing market.

China and North America, the highest two areas within the Industrial Metallic 3D printing area, skilled YoY cargo declines of -8% and -6%, respectively. Nevertheless, despite poor cargo exercise, total steel 3D printer revenues have been 8% increased than in Q3 2022.

This income progress has been pushed by inflationary value will increase and rising reputation in costlier massive build-volume, multi-laser powder mattress fusion programs.

The 3D printing ‘laser wars’ have been initially propagated by Western 3D printer producers equivalent to Velo3D and Nikon SLM Options. Nevertheless, Chinese language corporations equivalent to Farsoon, Eplus3D and Xi’an Brilliant Laser Applied sciences have entered this area over the previous yr. Eplus3D’s newest steel 3D printer, the EP-M1550, incorporates a 1558 x 1558 x 1200 mm construct quantity, and will be configured with as much as 25 lasers.

Whereas the PBF market witnessed widespread cargo decline, Directed Power Deposition (DED) 3D printers carried out effectively in Q3 2023. CONTEXT factors to the current emergence of entry-level DED choices from corporations equivalent to Meltio as main this progress. Elsewhere, SPEE3D shipped seven WarpSPEE3D chilly spray-based 3D printers to Ukraine as a part of a US Division of Defence (DoD) initiative.

Midrange 3D printers outperform skilled programs

As with Industrial 3D printers, the Midrange {and professional} markets skilled declining cargo figures.

Q3 2023 noticed shipments of Midrange 3D printers fall by 5% YoY and a pair of% sequentially. In response to CONTEXT, this decline was considerably decreased by sturdy shipments of latest low-end PBF programs, primarily from Formlabs, and rising vat polymerization 3D printer shipments in China predominantly from UnionTech. Excluding Formlabs and UnionTech, shipments declined by 17%, with different key market leaders performing poorly. In reality, Midrange 3D printer shipments have been down by 17% for Stratasys, 28% for 3D Techniques, and 33% for MarkForged, in Q3 2023.

In response to CONTEXT, Formlabs has recognised challenges throughout the Midrange phase, including merchandise with new modalities and in new price-ranges in consequence. CONTEXT calls this portfolio-expansion tactic a ‘recipe for achievement,’ which can’t solely assist the innovating firm but additionally elevate the market as an entire.

The Skilled 3D printing market reported a 41% decline in 3D printer shipments in Q3 2023, the sixth consecutive quarter of YoY cargo decline and the third to see a drop of 30% or extra. In recent times, market leaders UltiMaker and Formlabs have supplied extra feature-rich merchandise at more and more increased value factors. CONTEXT reported that this tactic has been profitable previously, however has struggled throughout the current inflationary context.

Inside the Skilled market, demand has now shifted to cheaper, “ok” programs. All Skilled 3D printing distributors, apart from newcomer Nexa3D, witnessed double-digit YoY cargo decline in Q3 2023.

Desktop 3D printing cannibalize trade gross sales

In contrast to all different 3D printing segments, CONTEXT experiences that the entry-level 3D printer market witnessed cargo progress of 9% in Q3 2023. That is primarily attributed to those extra inexpensive 3D printers cannibalizing gross sales from Skilled programs.

In response to CONTEXT, finish market patrons are more and more decided that they will obtain comparable performance and outcomes from entry-level programs as they will from these in costlier markets.

Desktop 3D printers at the moment are discovering use inside dental, automotive, medical & healthcare, aerospace, jewellery, and client product purposes.As such, these 3D printers are not restricted to hobbyist and basic buyer use.

Chinese language corporations proceed to dominate the desktop 3D printer market. Creality reportedly stands ‘head and shoulders above’ different corporations by way of international market share. Progress throughout the FDM area is exemplified by Bambu Lab, which CONTEXT beforehand reported as taking “the private 3D printer market by storm.” Inside the desktop LCD 3D printer market, Elegoo is displaying sturdy progress.

Poor 3D printer shipments to proceed?

Total, regardless of poor 3D printer cargo figures in Q3 2023, Connery argues that 2023 “has set the stage for a rebound and 3D printer shipments look to speed up within the years to return.”

Connery notes that international rates of interest are prone to stay elevated by way of no less than the primary half of 2024, that means near-term industrial system shipments could stay stagnant. Nevertheless, CONTEXT experiences that fears of regional recessions have largely abated, with the elemental worth of additive manufacturing being effectively acknowledged. That is set to clear the best way towards accelerated progress, as soon as the price of capital lowers within the second half of 2024 and into 2025.

Furthermore, Connery believes that the merger and acquisition exercise of 2023 will proceed into 2024. “Though the market could seem to have settled after the very public failed mergers of 2023, many corporations have overtly acknowledged that they’re extra privately investigating strategic options, that means that gross sales, mergers, acquisitions and divestitures could but lie forward.”

As 2023 drew to a detailed, Nano Dimension submitted a renewed supply for Stratasys. Elsewhere, different corporations equivalent to BigRep introduced plans to go public in 2024. Connery added that the Entry-level phase is “ripe for funding,” with extra corporations now recognising the rising worth supplied by this market.

Subscribe to the 3D Printing Business e-newsletter to maintain updated with the newest 3D printing information. You may as well observe us on Twitter, like our Fb web page, and subscribe to the 3D Printing Business Youtube channel to entry extra unique content material.

Are you curious about working within the additive manufacturing trade? Go to 3D Printing Jobs to view a number of obtainable roles and kickstart your profession.

Featured picture exhibits The Bambu Lab X1-Carbon 3D printer. Picture through Bambu Lab.